Copyright © mazanek.ch. All rights reserved.

Website made with love by PandaDesign

I own a property in Valais that is part of my private assets. What happens from a tax perspective if I sell it ?

In Switzerland, each canton is free to set the tax rules for real estate gains, within the limits of the law (Art. 12 LHID). The Confederation, for its part, does not levy any tax; private gains are exempt.

Profits from the sale of private real estate are taxed separately from other ordinary income. These profits are subject to “real estate gains tax” at a decreasing rate based on the number of years the property has been owned and the amount of the taxable profit.

At the time of sale, each owner receives an individual tax return to complete and return to the Tax Office. As soon as the tax is assessed, the Tax Administration sends the tax slip for payment.

Determining Taxable Profit

Generally, the taxable profit is calculated based on the sale price, from which the following expenses are deducted:

When the property has been owned for many years and it is not possible to justify the purchase price or construction cost, the Tax Administration may base its assessment on the cadastral value of the property. In this case, improvement expenses cannot be claimed. In certain special cases, it is possible to obtain an official appraisal of the property at the time of sale. This value will serve as the basis for calculation, replacing the purchase price.

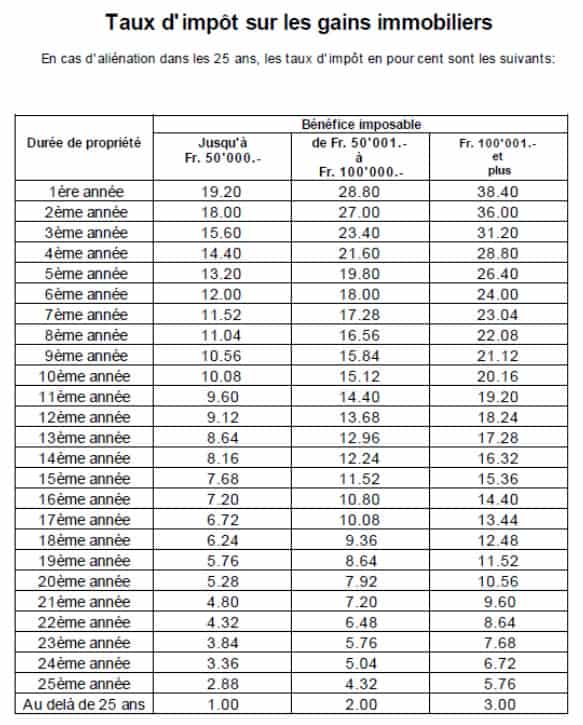

Number of years used to determine the tax rate

In Valais, taxable income is subject to the following scales :

Some special situations

How am I taxed if I received the property by gift ?

When the property was acquired free of charge, the number of years of ownership is calculated from the date the original donor became the owner of the property. In other words, if Person X acquired the property in 1980, it was transferred to his son in 2001, and the latter sold it in 2015, the relevant purchase date is 1980, not 2001. There is no tax on real estate gains at the time of the free acquisition, whether by inheritance or gift.

Depending on the family relationship between the former and new owners, gift or inheritance tax may, however, be levied.

My partner and I are divorcing, and she alone retains the family home, which we each own half. Do we have to pay tax ?

Generally speaking, property transfers between spouses do not generate any tax. In the event of a divorce, if one spouse retains sole ownership of the property, no tax will be levied at the time of the transfer. In the event of a subsequent resale, the determining date for calculating the length of ownership of the property will be the date of purchase or construction by the spouses, not the date of the change of ownership.

For example, Mrs. and Mr. X purchased a villa in equal shares in 1984. In 2010, the spouses divorced. The villa was retained by Mrs. X. In return, she paid Mr. X half of the value of the house. No tax on real estate gains applies at the time of divorce, even if there is a change of ownership. Mrs. X resold the property in 2014. The period of ownership will then be calculated from 1984. The share paid to Mr. X upon the dissolution of the matrimonial property regime cannot be deducted from taxable income as an investment expense.

Deferred taxation: a solution to avoid paying tax ?

Article 46 of the Valais Tax Act (LF) exhaustively lists the situations in which tax deduction is deferred. Indeed, in certain cases, even if the tax is due, it will not be deducted immediately, even if the owner of the property changes. Aside from the situations mentioned in the previous chapter (gifts or inheritance, divorce, or transfer between spouses), other events allow for tax deferral.

An example is the sale of the primary residence and the subsequent purchase (or construction) of another primary residence to replace it. Article 46 lit. The Federal Act of 1998 states :

“Taxation is deferred:

…

e) in the event of the alienation of a dwelling (house or apartment) that has been used for the sole and permanent use of the alienator, provided that the proceeds thus obtained are allocated, within an appropriate period, to the acquisition or construction in Switzerland of a dwelling serving the same purpose.”

“Appropriate period” means a period of two years according to established case law.

Depending on the amount of profit from the sale of the dwelling, as well as the purchase or construction price of the second dwelling, the tax may be deferred in full or in part. If the requirements are met, no tax, or only a partial tax, is levied upon the sale of the first property. Subsequently, upon the sale of the second property, if the conditions for deferred taxation are no longer met, the determining date for calculating the length of ownership will be the purchase date of the first property. If, on the other hand, these conditions are still met, tax payment will be deferred again.

Note that deferred taxation can only be applied to transactions related to the taxpayer’s primary residence. Second homes or rental properties do not fall into this category.